Global Skin Grafting Device Market Grows Rapidly Owing to Regenerative Therapies

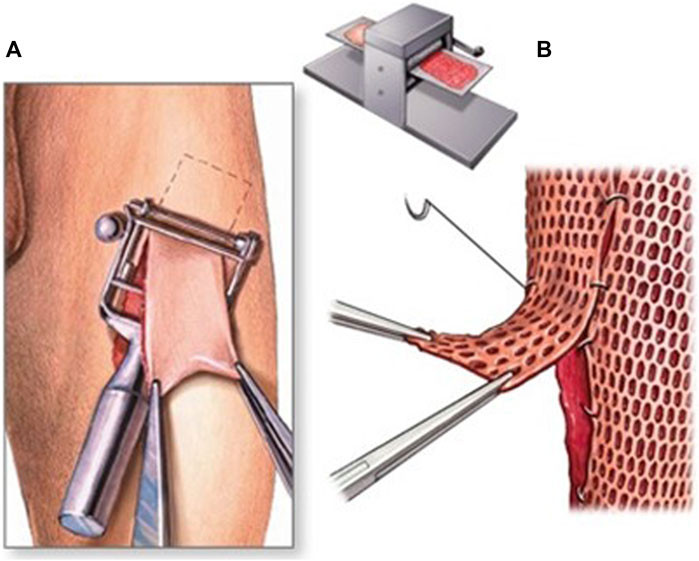

The Global Skin Grafting Device Market encompasses a range of surgical instruments and systems designed for harvesting, meshing, and implanting skin grafts in patients with burns, chronic wounds, and reconstructive surgery needs. These devices include dermatomes, meshers, fixation tools, and application kits that enable precise tissue removal and uniform graft distribution. Advantages of skin grafting devices include faster wound closure, minimized donor site trauma, reduced scarring, and lower infection risk, which collectively improve patient outcomes and shorten hospital stays.

The growing prevalence of diabetic foot ulcers, pressure sores, and severe burn injuries underscores the need for innovative Global Skin Grafting Device Market solutions. Moreover, an aging population and rising healthcare expenditure have propelled demand for regenerative therapies and advanced wound care. Ongoing research into biomaterials and personalized grafting techniques further highlights the market’s potential.

The skin grafting device market size is expected to reach US$ 1,519.0 million by 2032, from US$ 1084.9 million in 2025, at a CAGR of 7.3% during the forecast period.

Key Takeaways

Key players operating in the Global Skin Grafting Device Market are:

-Avita Medical

-Smith & Nephew

-MiMedx Group

-Organogenesis

-Zimmer Biomet

Driven by a surge in chronic wound cases and burn injuries, the market is experiencing robust growth in demand for skin grafting solutions. Rising incidence of diabetes, trauma, and venous leg ulcers is expanding the patient pool requiring grafts. Increased focus on reducing hospital stays and overall treatment costs has led healthcare providers to adopt efficient meshing devices and automated graft preparation systems. This trend is further amplified by growing healthcare infrastructure in emerging economies, shifting market dynamics, and rising market share of key device manufacturers.

Technological advancement remains a pivotal force shaping the competitive landscape. Innovations in regenerative medicine, such as bioengineered skin substitutes, growth factor–infused scaffolds, and 3D-printed graft matrices, are stepping up the market’s evolution. Portable meshing systems with digital controls and laser-guided dermatomes are improving precision and ease of use. Ongoing market research and investment in tissue engineering are expected to yield next-generation devices that offer enhanced biocompatibility and faster integration with host tissue.

Market Trends

One prominent trend is the integration of automation and robotics in skin grafting procedures. Automated meshing devices and robotic-assisted dermatomes enhance consistency, reduce manual error, and optimize graft thickness. These solutions align with broader industry trends emphasizing minimally invasive techniques and precision surgery.

Another key trend is the rise of personalized regenerative therapies and bioengineered skin substitutes. Advances in 3D bioprinting allow for patient-specific graft constructs using autologous cells and tailored biomaterial scaffolds. This approach supports faster healing, lowers rejection risk, and reflects the shift toward individualized treatment plans in wound care.

Market Opportunities

Expansion into emerging markets presents a significant opportunity for growth. Improving healthcare infrastructure, increased government initiatives for wound care management, and rising disposable incomes in regions such as Asia-Pacific and Latin America are fueling demand for advanced skin grafting devices. Local partnerships and distribution networks can help market companies penetrate these high-potential markets.

Another opportunity lies in strategic collaborations between device manufacturers and biotechnology firms to co-develop novel biomaterials and growth-factor delivery systems. By combining expertise in tissue engineering with device design, companies can introduce next-generation grafting kits that offer superior healing outcomes. Such alliances also enhance market research capabilities and accelerate product innovation.

Impact of COVID-19 on the Global Skin Grafting Device Market

The onset of the COVID-19 pandemic disrupted elective procedures and strained hospital resources worldwide, significantly slowing market growth for skin grafting devices during the peak infection waves. Pre-COVID, steady demand was driven by rising incidence of chronic wounds and burn injuries, supported by well-established supply chains and routine surgical schedules. When travel restrictions and lockdowns came into place, many hospitals deferred non-urgent surgeries, creating a bottleneck in hospital inventory replenishment and challenging manufacturers with sudden production halts. Supply-chain interruptions, coupled with reduced access to operating theaters, represented key market challenges that forced device companies to reprioritize distribution strategies.

As vaccination campaigns gained traction and healthcare systems adapted, post-COVID dynamics shifted toward recovery. Hospitals focused on clearing procedure backlogs, leading to a resurgence in procedures that utilize skin grafting tools. Digital consultations and remote monitoring platforms emerged to triage wound-care patients, highlighting new market opportunities in tele-health compatible devices. At the same time, evolving regulatory guidance around device sterilization and safety protocols added complexity but also fostered innovation in disposable and single-use grafting kits.

Looking ahead, future strategies must factor in robust risk management and lean manufacturing to handle sudden disruptions. Manufacturers are exploring regionalized production hubs to mitigate logistics risks and diversify supplier bases, a move that directly addresses supply chain resilience. Collaboration with contract research organizations and integration of real-world evidence will strengthen clinical acceptance and facilitate faster approvals. Embracing data analytics to track patient outcomes can enhance product portfolios and inform market insights for targeted launches. Firms that invest in modular device platforms, coupled with training programs for decentralized care settings, will be better positioned to capture long-term demand as operative volumes normalize and healthcare facilities prioritize value-based treatment pathways.

Regional Value Concentration in the Global Skin Grafting Device Market

North America maintains a dominant share in terms of market value, driven by advanced healthcare infrastructure, high procedural volumes, and favorable reimbursement frameworks for wound-care therapies. The United States accounts for the largest portion of industry revenue, with hospitals and specialized burn centers investing in next-generation skin grafting systems designed to improve patient recovery times. Europe follows closely, where mature markets such as Germany, France, and the UK exhibit strong adoption rates of both manual and automated grafting devices. Technological advancements and well-defined regulatory pathways in these countries contribute to the region’s robust market trends.

Asia Pacific represents the third major value pool, led by Japan, South Korea, and Australia. Although per-procedure spending is lower compared to Western markets, growing awareness of chronic wound management and increasing healthcare budgets in urban centers bolster regional demand. In contrast, Latin America and the Middle East & Africa regions hold smaller shares due to budget constraints and limited access to specialty healthcare services. Nonetheless, a gradual uptick in medical tourism and government initiatives to upgrade burn-care facilities offer promising market opportunities for device manufacturers seeking new revenue streams.

Cross-regional partnerships and strategic distribution alliances are common tactics to penetrate high-value territories. These efforts are underpinned by ongoing market research into payer policies and clinical guidelines, enabling companies to tailor product features to local procedural standards. As large hospitals continue to consolidate and form group purchasing organizations, economies of scale and negotiated pricing agreements further shape the competitive landscape in regions commanding the highest market revenues.

Fastest Growing Region in the Global Skin Grafting Device Market

Among all regions, Asia Pacific is currently the fastest growing market for skin grafting devices. Rapid urbanization, rising incidence of diabetic ulcers, and an expanding geriatric population are powerful market drivers in countries such as China and India. Both nations are investing heavily in healthcare infrastructure, including dedicated wound-care clinics and advanced burn-treatment centers. Favorable government initiatives to support indigenous manufacturing under “Make in India” and “Made in China 2025” frameworks have stimulated local production of grafting devices, improving affordability and accessibility.

Southeast Asia—particularly Indonesia, Malaysia, and Thailand—is also experiencing an upswing in demand. Growth is propelled by rising medical tourism, as these countries become hubs for cost-effective yet high-quality reconstructive surgeries. Portable and easy-to-use skin grafting systems gain traction in remote and rural clinics, bridging gaps in primary healthcare access. This shift is creating attractive market opportunities for companies offering scalable solutions with minimal training requirements.

Digital health integration further accelerates adoption in Asia Pacific. Telemedicine platforms that connect wound specialists with on-site clinicians enhance post-procedure monitoring, driving higher utilization of advanced skin grafting devices. Moreover, strategic collaborations between global device firms and local distributors enable rapid market penetration, leveraging existing networks to streamline regulatory approval and clinical validation.

Overall, the Asia Pacific region’s combination of favorable demographics, infrastructural investments, and supportive policy measures positions it as the fastest growing segment within the global skin grafting device market, presenting device manufacturers with significant avenues for expansion.

‣ Get More Insights On: Global Skin Grafting Device Market

‣ Get this Report in Japanese Language: 世界の皮膚移植機器市場

‣ Get this Report in Korean Language: 글로벌피부이식장치시장

‣ Resources- The Future of Skin Grafting: Global Skin Grafting Device

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

Comments

0 comment